Finding the perfect home requires a systematic approach that balances personal preferences with financial reality. Many buyers rush into viewings without establishing clear parameters, which leads to wasted time and emotional fatigue. A structured evaluation framework helps you filter listings efficiently while preserving your long-term financial stability. This guide outlines the exact steps to align your daily habits with your purchasing power and long-term goals. (About Team Pannell Real)

Assess Your Daily Habits and Neighborhood Preferences

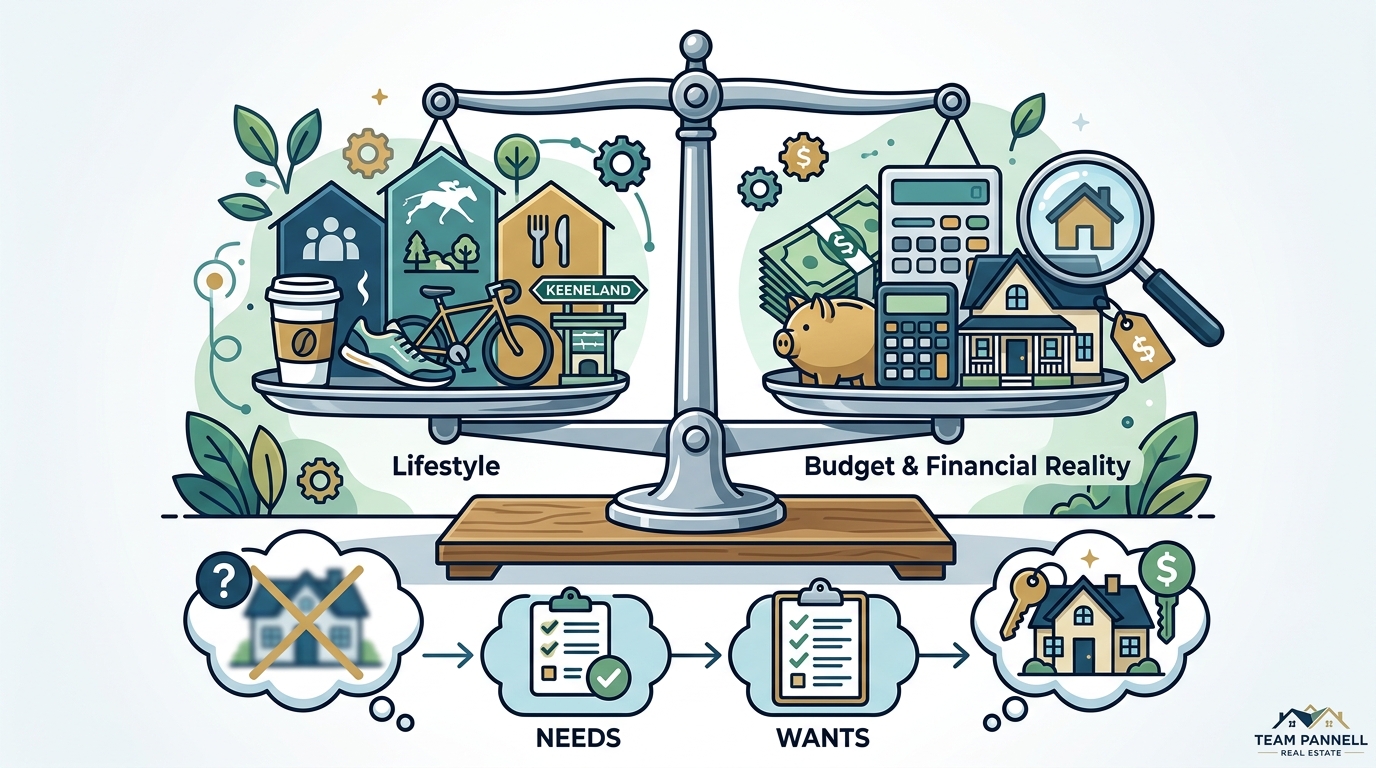

Start by mapping your routine activities onto a geographic grid. You must identify which amenities support your daily workflow and leisure time. Proximity to workplaces, schools, and recreational facilities directly impacts your long-term satisfaction. Neighborhood alignment is the systematic matching of daily routines with geographic proximity. You should prioritize areas that match your commute tolerance and social preferences. Lexington offers diverse districts that cater to distinct demographic needs. You can explore specific communities through our Andover Forest listings or browse our comprehensive community guides to understand local character.

Commute Analysis and Transit Access

Time spent traveling reduces your available leisure hours. Calculate the exact drive time during peak hours rather than relying on theoretical distances. You should factor in road construction schedules and seasonal traffic patterns. A reliable commute schedule prevents burnout and preserves family time. Many buyers overlook this metric until they have already purchased a home.

Amenity Proximity and Lifestyle Support

Identify the three to five locations you visit weekly. Map these points against available housing stock in your target price range. You will quickly discover which zip codes offer the best balance of convenience and cost. Convenience metrics directly correlate with daily happiness. Focus on districts that place your essential stops within a ten-minute radius.

Calculate Your Financial Boundaries and Mortgage Readiness

Financial clarity prevents emotional overspending during competitive bidding wars. You must establish a hard ceiling before you begin touring homes. Lenders typically evaluate your debt-to-income ratio and credit history to determine loan eligibility. Pre-approval letters are formal lender documents that verify your borrowing capacity. You should utilize our mortgage calculator to model different down payment scenarios. This step reveals your true purchasing power without hidden surprises.

Closing Costs and Hidden Expenses

Transaction fees often catch first-time buyers off guard. You must reserve additional capital for title insurance, appraisal fees, and transfer taxes. These expenses typically range between two and five percent of the final sale price. Planning for these upfront costs protects your emergency fund from depletion. Our closing cost guide breaks down every mandatory fee.

Maintenance Reserves and Long-Term Budgeting

Older homes require more frequent repairs and system replacements. You should allocate a monthly savings percentage specifically for property upkeep. Roof replacements, HVAC servicing, and landscaping demand consistent funding. Establishing a maintenance reserve ensures you never face financial distress after closing.

Evaluate Property Types and Structural Requirements

Structural preferences dictate your long-term maintenance burden and renovation potential. You must decide whether a move-in ready home or a fixer-upper aligns with your skill set and timeline. Property classification determines your renovation timeline and contractor availability. Single-family homes offer maximum privacy but require full yard management. Condos and townhomes reduce exterior maintenance but impose strict association rules. You can review our condo and townhome inventory to compare architectural styles.

Lot Size and Outdoor Utility

Land requirements vary drastically based on family size and hobby preferences. Large lots support gardening, pets, and outdoor entertainment setups. Smaller lots reduce mowing time and lower landscaping invoices. You should measure your actual outdoor usage before committing to acreage. Overestimating land needs often leads to paying for unused space.

Age and Condition Assessment

Construction era influences insulation quality, electrical capacity, and plumbing reliability. Pre-1980 homes often require complete system upgrades to meet modern standards. Newer developments typically include smart home integration and energy-efficient windows. You must weigh the immediate cash outlay against long-term utility savings. Our adding value framework helps you spot hidden renovation costs.

Navigate Local Markets and Community Amenities

Regional market dynamics shift rapidly based on interest rates and inventory levels. You must track how long properties remain active before receiving offers. Market velocity is the average number of days a listing remains active before receiving offers. Lexington features distinct micro-markets that operate on independent pricing curves. You can explore our Lexington market overview to understand current pricing trends. Working with local experts ensures you never overpay during inventory shortages.

School Districts and Future Resale Value

Education quality directly impacts long-term property appreciation. You should verify district boundaries before purchasing, as they rarely align with city limits. Strong academic programs attract consistent buyer demand during economic downturns. Even childless buyers benefit from the resale premium attached to top-rated zones. Our first-time buyer resources explain how to verify school performance metrics.

Community Governance and HOA Regulations

Homeowners associations enforce architectural standards and shared maintenance obligations. You must review the governing documents before signing any purchase agreement. Restrictive covenants can limit exterior paint colors, fence heights, and rental permissions. Understanding these rules prevents costly violations after you move in. Our seller and buyer guides provide checklists for reviewing association bylaws.

Conduct Strategic Viewings and Offer Preparation

Efficient property tours require a standardized scoring system. You should evaluate each home against your pre-defined lifestyle and budget criteria. Objective scoring eliminates emotional bias during competitive bidding. Bring a checklist that highlights structural flaws, neighborhood noise, and natural light patterns. You must photograph every room to compare properties side by side later. Our making an offer guide walks you through the submission process.

Inspection Negotiation and Repair Credits

Professional inspections reveal hidden defects that affect your long-term costs. You should request repair credits rather than demanding sellers complete work before closing. Sellers often lack the expertise to execute proper repairs, which creates future liability. Negotiating credits allows you to hire your preferred contractors at your own pace. Our escrow process explanation clarifies how funds are held during disputes.

Earnest Money and Contract Contingencies

Financial commitments demonstrate your seriousness while protecting your deposit. You must structure contingencies that allow you to exit the contract without penalty. Financing, appraisal, and inspection clauses provide essential escape routes. You should never waive critical protections unless the market conditions absolutely demand it. Our earnest money policy page details standard deposit percentages.

Property Comparison and Selection Matrix

Organizing your findings into a structured format prevents decision fatigue. You should compare at least three viable options before submitting any contracts. Side-by-side analysis highlights hidden trade-offs between price and features. The following matrix outlines the core differences between common housing categories.

| Property Category | Maintenance Responsibility | Privacy Level | Typical Buyer Profile |

|---|---|---|---|

| Single-Family Detached | Full owner responsibility | Maximum | Families seeking long-term stability |

| Condominium | Association manages exterior | Moderate | Professionals prioritizing convenience |

| Townhome | Shared wall maintenance | High | First-time buyers balancing cost and space |

| Luxury Estate | Full owner responsibility | Maximum | High-net-worth individuals seeking customization |

Key Takeaways

- Calculate your exact commute time during peak hours before selecting a zip code.

- Secure a pre-approval letter to establish your hard spending ceiling.

- Allocate two to five percent of the sale price for closing costs and transfer fees.

- Review homeowners association bylaws to avoid restrictive architectural violations.

- Use a standardized scoring system to eliminate emotional bias during tours.

- Request repair credits instead of demanding seller-completed renovations.

- Structure financing and inspection contingencies to protect your earnest money deposit.

Frequently Asked Questions

How do I determine my maximum affordable home price?

You should multiply your annual gross income by three or four, then subtract existing monthly debts. Lenders use this ratio to determine your loan eligibility and interest rate tier. You must also factor in property taxes, insurance, and maintenance reserves before finalizing your budget.

What is the average time to close on a Lexington home?

Transactions typically require thirty to forty-five days from contract acceptance to funding. This timeline allows lenders to complete appraisals, title searches, and final underwriting. You should schedule your moving company only after the closing documents are fully executed.

How do I evaluate neighborhood safety without relying on crime maps?

You must visit the area at different times of the day and week to observe foot traffic and lighting. Talk to local business owners and long-term residents about community engagement and maintenance standards. Safety perception directly impacts your daily comfort and long-term resale value. Look for well-maintained properties, active street lighting, and visible neighborhood watch signs.

When should I consider a fixer-upper versus a move-in ready home?

Fixer-uppers require substantial cash reserves and project management expertise. You should only pursue renovation projects if you have verified contractor bids and a realistic timeline. Move-in ready properties command higher upfront prices but eliminate immediate repair stress. Your decision should align with your available time and risk tolerance.

How do HOA fees impact my monthly housing budget?

Association dues cover shared amenities, landscaping, insurance, and reserve fund contributions. You must add these recurring payments to your mortgage calculation before submitting an offer. High HOA fees can significantly reduce your purchasing power in competitive markets. Always request the most recent financial statements to verify reserve adequacy.

What documents do I need to secure a mortgage pre-approval?

Lenders require recent pay stubs, W-2 forms, tax returns, and bank statements for the past two years. You must also provide documentation for any large deposits or outstanding debts. Complete documentation accelerates the underwriting process and strengthens your offer position. Our pre-approval guide lists every required financial record.

How do I handle multiple offers in a competitive market?

You should submit your strongest initial offer rather than waiting to escalate. Personalized letters, flexible closing dates, and minimal contingencies improve your standing. You must work with an experienced agent who understands local bidding patterns. Our strategic offer framework outlines proven tactics for winning bids.

Begin Your Property Search Today

Matching your lifestyle and budget requires disciplined research and expert guidance. You should schedule a consultation with our licensed agents to review your specific criteria. We provide personalized home search tools, market analysis reports, and negotiation support throughout the entire transaction. Visit our main homepage to access our full inventory and schedule your first property tour. Contact our Lexington office at (859) 800-6823 or our Nicholasville location at (859) 800-6548 to start your journey.